Technology firms continue to rip higher this year. The Nasdaq is already up over 18% so far this year. This is after a technology firms underperformed for quite some time even up through the first part of this year.

The tech story is a mirror image of the the Internet bubble of the late 90's. Today technology firms are growing rapidly, have superbly strong balance sheets, high free cash flow, high net income and they have nothing to do with mortgages or subprime.

But here is the best part. The large tech companies are huge beneficiaries of the global growth story. Google, Apple, Cisco, Hewlett Packard, Dell, Microsoft all have a very large percentage of their revenues come from international operations. The falling dollar is further enhancing these companies results.

We are experiencing an unprecedented global growth story around the world. All of these strong global economies need computers, software, telecommunications, search, etc. We are also in what is traditionally the strongest seasonal period for tech companies. I believe that tech will see a strong finish going into the end of the year.

Disclosure: at the time of this posting the author was long GOOG, AAPL, CSCO, HPQ, DELL, MSFT.

Wednesday, October 31, 2007

Year-End Stock Market Forecast

A number of people have asked me what I think the stock market will do the last part of 2007. There are really two markets right now: a continuing bull market in minerals and mining, energy, agriculture, technology, global infrastructure and emerging markets; a bear market in financials, home builders and anything touching the toxic slime of sub-prime mortgages.

I think it is more likely that the market will be higher by January 1st than lower. Even though the total return of the stock market has been very good this year, there continues to be a wall of worry the the credit and subprime mess, slowing U.S. economy and sky high oil and commodity prices will cause a sharp downturn in the market.

My understanding is that hedge funds have the highest short ratio that they've ever had. A lot of protection has also been purchased in the form of defensive put options. In addition, due to a lot of caution resulting from the sharp downturn in February and again in August, many market managers have underperformed the market. There are just a lot of people that have "hung back" this year.

I think it is more likely that the market will be higher by January 1st than lower. Even though the total return of the stock market has been very good this year, there continues to be a wall of worry the the credit and subprime mess, slowing U.S. economy and sky high oil and commodity prices will cause a sharp downturn in the market.

My understanding is that hedge funds have the highest short ratio that they've ever had. A lot of protection has also been purchased in the form of defensive put options. In addition, due to a lot of caution resulting from the sharp downturn in February and again in August, many market managers have underperformed the market. There are just a lot of people that have "hung back" this year.

Why is all of this important? Because it means that there is a lot of money that is available to come into the market on the long side. Money managers that have underperformed are going to have to chase performance going into the end of the year. They won't have any choice but to pile into the stocks that are still going up. People that have been overly cautious may very likely rush into the market as it continues to get away from them.

Trades that should be working, like shorting VMWare while being long EMC are not working, as VMWare just goes up and up. People that don't remember how rapid and brutal an emerging market correction can be are pouring money into China, further inflating the bubble. All of this leads me to believe that themes that have been working will continue to work in the race to the end of the year. And you know what? Bubbles can continue to inflate for a long time before the inevitable implosion comes.

Oil sure looks toppy. I have lightened up on some of my energy positions believing that there could be a correction sooner rather than later. Refiners and integrated oil companies have not done as well lately due to the very narrow cracking spreads. The crack spread should widen as we get further into winter helping the refiners' margins.

I've heard some prognosticators suggest that financials are in position for a strong move up since they have been so beaten up. But I think there are so many other good ideas that are continuing to work why should I take a chance on Citigroup and the risk that a few more billion of bad SIV's crawl out from under its balance sheet?

The economy had slowed but there hope of a soft landing and reacceleration. The just released 3rd quarter's GDP number showed growth of 3.9% - the strongest performance in 4 years. Employment remains strong. Real wages are growing. Disposable income in real terms has increase 4.7% in the past year. Inflation is in check.

The Dollar continues to fall but American exports are surging and imports are falling, significantly reducing the current account deficit. The housing downturn took a bite out of last quarter's GDP number but the increase in exports put back in almost exactly the same amount.

The Federal Reserve just cut the overnight lending rate by 25 basis points as an insurance policy. The Fed may cut another 25 basis points in December but we are getting closer to neutral.

Assuming I'm right I can certainly see a significant downturn early in 2008 due to tax gain selling after a big 2007. Hopefully I will be one of them.

Disclosure: at the time of this posting the author was long VLO, EMC, DVN, LFC, CHL and short POT, XOM, USO.

Tuesday, October 30, 2007

A Legacy of Alarmism - From Malthus to Gore

In the mid-nineteenth century Malthusian theory predicted the mass starvation of the world's population because the number of people would increase faster than the food supply. In the last 150 years the planet has increased from 1B to 8B souls. There are plenty of problems with the distribution of food around the world. But I suspect that about the same percentage of the world's population is hungry that was 150 years ago.

Karl Marx predicted that the proletariat would rise up and create a worker's utopia. Marx was wrong (and dead to boot - Castro to join him in hell shortly).

The Democrats of the 1960's predicted that the world was destined for a nuclear winter and a "Mad Max" scenario.

The Club of Rome predicted 30 years ago that the world would soon run out of energy resulting in economic collapse.

This year Al Gore won an Oscar and the Nobel Peace Price for a movie that scientists who actually study the environment for a living, and specifically the composition of the atmosphere and the effect of changes on it, say is preposterous nonsense.

Never underestimate the will of humans to survive and the inventiveness of people to solve the next problem facing the planet - or the fact that alarmism will always be alive and well.

Karl Marx predicted that the proletariat would rise up and create a worker's utopia. Marx was wrong (and dead to boot - Castro to join him in hell shortly).

The Democrats of the 1960's predicted that the world was destined for a nuclear winter and a "Mad Max" scenario.

The Club of Rome predicted 30 years ago that the world would soon run out of energy resulting in economic collapse.

This year Al Gore won an Oscar and the Nobel Peace Price for a movie that scientists who actually study the environment for a living, and specifically the composition of the atmosphere and the effect of changes on it, say is preposterous nonsense.

Never underestimate the will of humans to survive and the inventiveness of people to solve the next problem facing the planet - or the fact that alarmism will always be alive and well.

Counting the Cockroaches at Merrill Lynch

I believe that Merrill Lynch, and probably some of the other big financial institutions, don't fully understand the extent of their losses in Structured Investment Vehicles (SIV). I previously commented that the fact that Merrill Lynch increased their write-off from $5B to $8.4B in a week shows that they are guessing - marketing to model. It reminds me of the old adage that if you see one cockroach there are many, many more that you don't see.

The real danger to the shareholders is that there is no way of knowing how deep Merrill Lynch is into this mess. Much of their SIV holdings are hidden in off-balance sheet accounts - some that have been moved off shore for further secrecy. No ones knows how many billions of dollars in SIV's are held by Merrill Lynch and what mix of mortgage securities are backing these SIV's.

The tipping point appears to have been last summer, when 3 senior executives were fired by Merrill Lynch. It was reported by CNBC today that at this point Merrill Lynch's mortgage backed securities portfolio stood at about $2B. Subsequently the firm expanded its SIV exposure dramatically, from as low as $20B to what some have speculated was as high as $40B.

Merrill Lynch fired its CEO today. Maybe "fired" is a bit strong a word, since Stanley O'Neil received $161M in compensation for leaving. Clearly Mr. O'Neil did a terrible job in allocating capital and managing risk. But at this point the Board of Directors has a fiduciary responsibility to the shareholders to shine a bright light in the dark room of off-balance sheet shenanigans.

Mr. O'Neil should receive credit for the fact that he was instrumental in turning Merrill Lynch around after it fell into hard times a few years ago. Nevertheless it is his responsibility that Merrill Lynch took the leading role on Wall Street in dealing these CDO's.

I thought the whole point of the post-Enron reforms was to make sure that opaque off-balance sheet debts would not be allowed. The SEC is absent as usual. The government's proposal to create the enormous pool of shared securities will only keep these SIV's off the books of the big firms, and that is wrong.

Wall Street is stumbling around with no idea about how to price this stuff. I predict we will see further write downs for the next several quarters as a result of this mess.

The real danger to the shareholders is that there is no way of knowing how deep Merrill Lynch is into this mess. Much of their SIV holdings are hidden in off-balance sheet accounts - some that have been moved off shore for further secrecy. No ones knows how many billions of dollars in SIV's are held by Merrill Lynch and what mix of mortgage securities are backing these SIV's.

The tipping point appears to have been last summer, when 3 senior executives were fired by Merrill Lynch. It was reported by CNBC today that at this point Merrill Lynch's mortgage backed securities portfolio stood at about $2B. Subsequently the firm expanded its SIV exposure dramatically, from as low as $20B to what some have speculated was as high as $40B.

Merrill Lynch fired its CEO today. Maybe "fired" is a bit strong a word, since Stanley O'Neil received $161M in compensation for leaving. Clearly Mr. O'Neil did a terrible job in allocating capital and managing risk. But at this point the Board of Directors has a fiduciary responsibility to the shareholders to shine a bright light in the dark room of off-balance sheet shenanigans.

Mr. O'Neil should receive credit for the fact that he was instrumental in turning Merrill Lynch around after it fell into hard times a few years ago. Nevertheless it is his responsibility that Merrill Lynch took the leading role on Wall Street in dealing these CDO's.

I thought the whole point of the post-Enron reforms was to make sure that opaque off-balance sheet debts would not be allowed. The SEC is absent as usual. The government's proposal to create the enormous pool of shared securities will only keep these SIV's off the books of the big firms, and that is wrong.

Wall Street is stumbling around with no idea about how to price this stuff. I predict we will see further write downs for the next several quarters as a result of this mess.

The Impact of High Oil Prices

The price of oil has become disconnected from the economics of supply and demand. There is a risk premium due to geopolitical events: tension between Turkey and the Kurds, a potential military strike of take out Iran's nuclear capability. We are an event or two from $100 oil.

Long term oil will go higher based on the depreciation of the dollar and continued strong growth of the world's economies. Nevertheless I b elieve there is a better chance that it will go lower in the short term.

elieve there is a better chance that it will go lower in the short term.

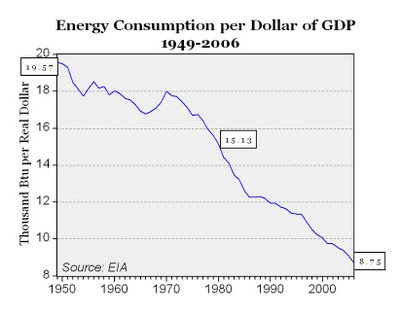

The difference between former "oil shocks" is that this one is based largely on demand due to strong economic growth rather than a constraint on supply. Yesterday, oil finally surpassed its all time high from 1979 in constant dollar terms. But higher oil prices do not have the same impact on our economy that they once did. A big reason is that we are so much more productive and so much more energy efficient that we were in decades past.

There was a terrific discussion on last night's Kudlow & Company on CNBC on the price of oil and its impact. This chart is from that program. Today it takes well less than half the energy it took in 1949 to produce a dollar of GDP. It takes just over half the energy to produce a dollar of GDP than it did even 26 years ago in 1980. This is dramatic progress in terms of efficient use of energy. The result is that our economy relies far less on energy to produce GDP than we did even several decades ago.

Disclosure: at the time of this posting the author was long DVN, VLO, CCJ and short USO.

Long term oil will go higher based on the depreciation of the dollar and continued strong growth of the world's economies. Nevertheless I b

elieve there is a better chance that it will go lower in the short term.

elieve there is a better chance that it will go lower in the short term.The difference between former "oil shocks" is that this one is based largely on demand due to strong economic growth rather than a constraint on supply. Yesterday, oil finally surpassed its all time high from 1979 in constant dollar terms. But higher oil prices do not have the same impact on our economy that they once did. A big reason is that we are so much more productive and so much more energy efficient that we were in decades past.

There was a terrific discussion on last night's Kudlow & Company on CNBC on the price of oil and its impact. This chart is from that program. Today it takes well less than half the energy it took in 1949 to produce a dollar of GDP. It takes just over half the energy to produce a dollar of GDP than it did even 26 years ago in 1980. This is dramatic progress in terms of efficient use of energy. The result is that our economy relies far less on energy to produce GDP than we did even several decades ago.

Disclosure: at the time of this posting the author was long DVN, VLO, CCJ and short USO.

Sunday, October 28, 2007

Investments I'm No Good At

Pharmacuticals - I've made some money but always seem to behind the "8-ball" in this sector. My latest attempt: I bought Celgene last week.

Semiconductors - this sector is impossible for me; nothing but suprises to the downside.

Day Trading - but I do very well with month trading sometimes when I see a good idea - but trying to guess on day trades is not my thing.

And of course, any day the market is open is a good day to sell airline stocks.

Disclosure: at the time of this posting the author was long DNA, AMGN and CELG.

Semiconductors - this sector is impossible for me; nothing but suprises to the downside.

Day Trading - but I do very well with month trading sometimes when I see a good idea - but trying to guess on day trades is not my thing.

And of course, any day the market is open is a good day to sell airline stocks.

Disclosure: at the time of this posting the author was long DNA, AMGN and CELG.

GOP Principles vs. Democratic Policy Wonks

Recently Dave Helfert, a former Appropriations spokesman who now works for Rep. Neil Abercrombie (D-Hawaii) sent out a memo to all Democrat House press secretaries and communications directors detailing his frustrations with the Democratic message.

The gist of his concern was that the GOP almost always wins the Washington war of rhetoric. While the Republicans craft messages that are simple, clear and based on well understood principles the Democrat's messages all seem like they were put together by policy wonks.

Helfert's memo "got out" as these things will do. Brian Kennedy, spokesman for House Minority Leader John Boehner (R-Ohio), bemusedly stated that, “House GOP communicators would take his remarks as a compliment.”

Apparently the staff of the House Democratic Caucus, which is responsible for setting the Democratic message, were “a little less than pleased.”

Dave Helfert's has a track record of being extremely critical of the Bush Administration and its policies. But his memo also implies that the GOP's successful rhetoric is aided by neurological response. By using emotional appeals and warning of dire threats, Republicans can trigger neurons called “amygdalae” in the temporal lobe, which is the seat of the “fight or flight” response in the brain.

“Almost every Republican message contains a simple and direct moral imperative, a stark contrast between good and evil, right and wrong, common sense and fuzzy liberal thinking,” states Helfert's memo. “Meanwhile, we’re trying to ignite passions with analyses of optimum pupil-teacher ratios.”

I'm no neurologist, and don't know much about "amygdalae", but I do think Helfert is onto something. Crafting messages that work is easier for the Republicans than for the Democrats. The reason is that Republicans believe in principles and logic and facts while the Democrats think in terms of policy and emotion.

Principles and logic and facts make it very easy to craft messages that are exactly as Helfert complains about: "simple and direct moral imperative, a stark contrast between good and evil, right and wrong, common sense and fuzzy liberal thinking." I'm not sure a GOP strategist could have said it any better!

Fortunately the facts and logic do not typically support Democratic positions. It makes the rhetorical war a bit one sided. Bringing an emotional argument to a factual debate is a lot like bringing a knife to a gunfight.

The gist of his concern was that the GOP almost always wins the Washington war of rhetoric. While the Republicans craft messages that are simple, clear and based on well understood principles the Democrat's messages all seem like they were put together by policy wonks.

Helfert's memo "got out" as these things will do. Brian Kennedy, spokesman for House Minority Leader John Boehner (R-Ohio), bemusedly stated that, “House GOP communicators would take his remarks as a compliment.”

Apparently the staff of the House Democratic Caucus, which is responsible for setting the Democratic message, were “a little less than pleased.”

Dave Helfert's has a track record of being extremely critical of the Bush Administration and its policies. But his memo also implies that the GOP's successful rhetoric is aided by neurological response. By using emotional appeals and warning of dire threats, Republicans can trigger neurons called “amygdalae” in the temporal lobe, which is the seat of the “fight or flight” response in the brain.

“Almost every Republican message contains a simple and direct moral imperative, a stark contrast between good and evil, right and wrong, common sense and fuzzy liberal thinking,” states Helfert's memo. “Meanwhile, we’re trying to ignite passions with analyses of optimum pupil-teacher ratios.”

I'm no neurologist, and don't know much about "amygdalae", but I do think Helfert is onto something. Crafting messages that work is easier for the Republicans than for the Democrats. The reason is that Republicans believe in principles and logic and facts while the Democrats think in terms of policy and emotion.

Principles and logic and facts make it very easy to craft messages that are exactly as Helfert complains about: "simple and direct moral imperative, a stark contrast between good and evil, right and wrong, common sense and fuzzy liberal thinking." I'm not sure a GOP strategist could have said it any better!

Fortunately the facts and logic do not typically support Democratic positions. It makes the rhetorical war a bit one sided. Bringing an emotional argument to a factual debate is a lot like bringing a knife to a gunfight.

Another Frustrating Stock I Own - Toyota Motors

I began investing in TM early this year with it trading at about $130 per ADR (the ADR equals 2 TM shares). After getting as high as $138 it last week went below $105. On the way down I have bought LEAP calls, sold LEAP puts and sold short term puts. I have made money on a number of the short term puts but overall am so far underwater I need a periscope. Friday's close was just north of $110.

I believe the Toyota ADR is worth $165 a share. This is a company that will only increase its dominance of the auto industry over the next decade. Why is the stock struggling? I believe there are several reasons. First, The economic slowdown in the U.S., 40% of Toyota's revenue, is problematic. The housing and credit troubles raise concerns about auto sales being negatively impacted. There are fears that the credit problems will start to crop up in auto loans.

Second, the Yen continues to hold even with the dollar even as the Dollar continues to depreciate against other foreign currencies such as the Euro. A strengthening Yen will have a negative impact on Toyota's top and bottom line numbers.

Although the Bank of Japan continues to keep interest rates at 0.5% there is concern that the Yen carry trade may suddenly unravel. If that were to happen a lot of money managers would have to buy large quantities of Yen, driving the value of the Yen up against the Dollar. Also, if the Bank of Japan decided to begin raising interest rates the Yen in all probability would strengthen.

But lets look at the positives for Toyota. Toyota continues to gain market share almost every month against the America automakers. Last month was an anomaly in that General Motors' U.S. sales increased slightly while Toyota's sales declined by 4%. However Ford's sales declined 21% for the month (year over year) after a more than 30% decline the month before.

Toyota is immensely profitable vis a vis its American and other global counterparts. Last year Toyota Motors made twice as much profit as Ford, GM and Honda Motors combined.

I believe the Toyota ADR is worth $165 a share. This is a company that will only increase its dominance of the auto industry over the next decade. Why is the stock struggling? I believe there are several reasons. First, The economic slowdown in the U.S., 40% of Toyota's revenue, is problematic. The housing and credit troubles raise concerns about auto sales being negatively impacted. There are fears that the credit problems will start to crop up in auto loans.

Second, the Yen continues to hold even with the dollar even as the Dollar continues to depreciate against other foreign currencies such as the Euro. A strengthening Yen will have a negative impact on Toyota's top and bottom line numbers.

Although the Bank of Japan continues to keep interest rates at 0.5% there is concern that the Yen carry trade may suddenly unravel. If that were to happen a lot of money managers would have to buy large quantities of Yen, driving the value of the Yen up against the Dollar. Also, if the Bank of Japan decided to begin raising interest rates the Yen in all probability would strengthen.

But lets look at the positives for Toyota. Toyota continues to gain market share almost every month against the America automakers. Last month was an anomaly in that General Motors' U.S. sales increased slightly while Toyota's sales declined by 4%. However Ford's sales declined 21% for the month (year over year) after a more than 30% decline the month before.

Toyota is immensely profitable vis a vis its American and other global counterparts. Last year Toyota Motors made twice as much profit as Ford, GM and Honda Motors combined.

Bob Nardelli will likely run Chrysler into the ground the way he did Home Depot. John Snow, former Treasury Secretary and the head of Cerberus Capital, hired Bob Nardelli. As Treasury Secretary John Snow did not impress has being the sharpest knife in the drawer.

Toyota is making strong inroads into China, as is General Motors. Finally there is valuation. Toyota sells for a P/E of 11.38. On every valuation metric Toyota stands alone in the automotive industry. I suppose that Honda may have a premium valuation due to the fact that it is smaller and may be able do better regarding the law of large numbers. But I think Toyota is going to rule the automotive world. They are making steady process in competing for the full size truck, the last segment of dominance of U.S. car makers.

Toyota has more than 10% of the value of its shares in cash. In fact, Toyota can afford to pay cash for General Motors given GM's market cap and Toyota would have some change left over.

Hopefully Toyota will move up as we continue to gain more clarity on the credit mess and whether the U.S. economy will re-accelerate into 2008.

Direct Competitor Comparison statistics a re from Yahoo Finance.

re from Yahoo Finance.

Disclosure: at the time of this posting the author was long TM.

Saturday, October 27, 2007

Tax Plan & the Media's Lazy Absence of Analysis

http://www.ajc.com/metro/content/printedition/2007/10/26/taxes1026.html

The above link is an Associated Press article describing the tax plan proposed by Charlie Rangel, Democrat Chairman of the House Ways and Means Committee. This is the article that was picked up by most newspapers that do not have the resources to research and write the article themselves. This includes all but the largest newspapers such as the New York Times. The link is from the print edition of the Atlanta Journal Constitution. So most people's print understanding of the proposal comes from this article.

It is a great example (in a sorry sort of way) of how the media passes on the Democratic message without any true analysis or skepticism. Rush Limbaugh calls it the "drive by media" due to the superficial nature of coverage combined with a natural tendency to accept what the Democrats say as good and true. The media is just lazy.

To read the article without any other source of information the reader is left believing the the following:

What has John Abrams of the AP left out? Well, here are a few items:

The above link is an Associated Press article describing the tax plan proposed by Charlie Rangel, Democrat Chairman of the House Ways and Means Committee. This is the article that was picked up by most newspapers that do not have the resources to research and write the article themselves. This includes all but the largest newspapers such as the New York Times. The link is from the print edition of the Atlanta Journal Constitution. So most people's print understanding of the proposal comes from this article.

It is a great example (in a sorry sort of way) of how the media passes on the Democratic message without any true analysis or skepticism. Rush Limbaugh calls it the "drive by media" due to the superficial nature of coverage combined with a natural tendency to accept what the Democrats say as good and true. The media is just lazy.

To read the article without any other source of information the reader is left believing the the following:

- The plan will provide "tax cuts to almost all families with incomes under $500,000."

- Rich people, implied to be families that make more than $500,000 a year, will pay somewhat higher taxes.

- Rich families will be subject to a phase-out of deductions and exemptions.

- The corporate tax will be lowered from 35% to 30.5%. Some companies will have to pay a little more.

- $29B in additional money will be paid out through the earned income tax credit (not a tax reduction as the recipients don't pay taxes)

- $9B in additional child credits will be paid out.

- The Alternative Minimum Tax will be eliminated.

- 91 million families will receive tax relief.

What has John Abrams of the AP left out? Well, here are a few items:

- Families making over $200,000 a year will pay a 4% "surcharge". This surcharge will be against total income instead of taxable income which means it will subtract from all itemized deductions such as the mortgage deduction. So it is actually a bigger hit than 4%.

- The marginal rates will be raised from including raising the top marginal rate 35% to 39.5%. This tax rate increase is separate from the 4% surcharge. The surcharge is on top of this.

- I'm not sure what John Abrams means by saying that the rich will be subject to "a limitation on itemized deductions and a phase-out of deductions for personal exemptions." I can't imagine what these might be. If you make more than $200,000 as a family most of the deductions are already phased out. Then the AMT eliminates much of everything else. Since this phase-out will raise $29B for the government I can only assume that Rangel is integrating many of the AMT deduction caps into the mainline tax code.

- Carried interest, which is the capital gain that is paid to hedge fund and private equity managers as pay for performance, will be redefined as ordinary income raising the tax rate on these gains from 15% to 44%.

- A number of other measures will be enacted pulling in many tens of billions from companies.

- The 91 million receiving tax cuts number is smoke and mirrors. 20M are have already been shielded from the AMT by a previous GOP patch. Many more millions only receive a "cut" if you assume that the 10% rate expires and that the $1,000 child credit expires (both provided through the GOP tax cuts of 2001 and 2003). Others that will benefit from expanding the earned income tax credit don't actually pay taxes. We're just going to redistribute more income to them.

Off-Balance Sheet, Off-Shore, Offensive

Merrill Lynch and a number of the other big New York financial institutions made the mistake of taking huge risks on Structured Investment Vehicles (SIV's) for the potential reward of a modest return but not hedging the downside. These CEO's have been paid enormous sums of money to make money and manage risk. It is becoming very clear that, with the exception of Goldman Sachs, risk was not managed.

Merrill Lynch stated a week ago that they would take a $5B hit on their sub-prime and SIV's. Then when they released their earnings it had turned into a $8B write-down. This is for a firm that makes maybe $6B in profits in a year.

The fact that it went from $5B to $8B in the course of a week tells us that they have no idea what the ultimate hit will be. It shows that they are still not marking to market but are marking to model. I suppose they took another look at their model and decided that the write-down should include and additional $3B. But instead of $5B or $8B it could be $10B or who knows what.

Perhaps even scarier Merrill Lynch and others are hiding their SIV assets in off-balance sheet entities. Some of these off-balance sheet entities have even moved off-shore for even greater opaqueness. This is exactly the type of fraud that was perpetrated by Enron, hiding huge losses off its balance sheet until it was too late for the firm to stop its ultimate collapse.

Where is the SEC? Absent as usual. Without Eliott Spitzer as New York Attorney General to do the SEC's job for them, the SEC continues to be the feckless, financial statement collecting bureaucrats that they always have been.

Not a single one of these CEO's that failed their shareholders by not managing risk has been fired. No government investigation is underway to reveal what is being hidden in these off-balance sheet entities. It is appalling.

Disclosure: at the time of this posting the author was long GS.

Merrill Lynch stated a week ago that they would take a $5B hit on their sub-prime and SIV's. Then when they released their earnings it had turned into a $8B write-down. This is for a firm that makes maybe $6B in profits in a year.

The fact that it went from $5B to $8B in the course of a week tells us that they have no idea what the ultimate hit will be. It shows that they are still not marking to market but are marking to model. I suppose they took another look at their model and decided that the write-down should include and additional $3B. But instead of $5B or $8B it could be $10B or who knows what.

Perhaps even scarier Merrill Lynch and others are hiding their SIV assets in off-balance sheet entities. Some of these off-balance sheet entities have even moved off-shore for even greater opaqueness. This is exactly the type of fraud that was perpetrated by Enron, hiding huge losses off its balance sheet until it was too late for the firm to stop its ultimate collapse.

Where is the SEC? Absent as usual. Without Eliott Spitzer as New York Attorney General to do the SEC's job for them, the SEC continues to be the feckless, financial statement collecting bureaucrats that they always have been.

Not a single one of these CEO's that failed their shareholders by not managing risk has been fired. No government investigation is underway to reveal what is being hidden in these off-balance sheet entities. It is appalling.

Disclosure: at the time of this posting the author was long GS.

Finding the Next 5,000 Percent Gainer

Financial publications are fond of writing about the fabulous gains in great companies if you'd only gotten in early. Examples of stocks that would make you a millionaire if you bought early and just held on include Walmart, Microsoft, Home Depot to name just a few.

Microsoft provides a good case study. Microsoft peaked at $58 and change right at the end of 1999. Then came the collapse of the tech bubble. Microsoft has done nothing but go sideways for seven years. Finally on Friday Microsoft hit a six year high of $35 after reporting a superb quarter that showed all lines of business were executing exceptionally well.

Microsoft IPO'd about 1985. On a split adjusted basis a share of stock was worth 9.5 cents. From that point to the peak is a return of 6,110%. Many times people look at a stock that has moved strongly from the lower right to the upper left and feel that they've "missed the boat". If you'd bought Microsoft at the beginning of 1990 a share would have cost about $0.64. The stock would already have gone up 670%. But you would still have made a 910% return at the peak. If you bought Microsoft in 1995 a share would have cost $3.71 on a split adjusted basis. Over the next 5 years you would have a return of almost 160%, or an annualized return of 32% a year.

Somewhere today there is the next 5,000% stock. While hindsight is entertaining it is not particularly profitable. What are the characteristics of a stock that can return 5,000% over 15 or 20 years?

In the case of Microsoft it was a defensible franchise in a fast growing industry, personal computers. Microsoft's operating system dominance meant that they grew as the industry grew. Many additional products put out by Microsoft over the years, such as Microsoft Office and Internet Explorer, have been successful and profitable in their own right, but essentially were developed to protect the core operating system franchise.

I own a lot of different stocks and I own them for a lot of different reasons. But of all the stocks I own the one that I think may turn in a Microsoft performance over the next 10 years is Google. Google IPO'd 3 years ago for $85 a share. I first bought Google in late 2006 for $410. At that time Google had already posted a return of 482%. Friday, Google's closing price was $674.60, representing an increase of 794% since the IPO.

Google has not split its shares and the high stock price along with concerns over the sustainability of its growth have meant that the shares have climbed a "wall of worry" and moved up in a rational way based on its continued strong earnings. The stock remained fairly flat last year and early this year. But with the latest quarter analysts are starting to become more comfortable that growth and earnings are not going to slow down precipitously - at least not in the foreseeable future.

Like Microsoft, Google has a dominate position and a defensible franchise in an industry that is expect to grow for a long time - search and Internet advertising. Google's search algorithms continue to improve and this latest quarter showed financial gains based on more accurately targeted advertising based on search results.

Like Microsoft, Google's business model generates huge amounts of free cash flow. This gives Google the ability to invest in widening its moat and invest in other products and services for future growth. Google has its fingers in a lot of pies, but they have been disciplined in that most of these initiatives are either meant to defend the core franchise (like Microsoft realizing that it had to win the Internet browser war), or meant to expand its footprint within the scope of it's stated mission. That mission is to organize the world's information and monetize the access of that information. There has been no move by Google that just doesn't fit, like Ebay's acquisition of Skype (which Ebay just took a massive write-down on).

Google is a global growth story with about 50% of its revenue coming from outside the United States. Google continues to gain market share in almost every market in which they compete. They are even gaining market share in the U.K. where their market share is already 70%.

It is much harder to see the future than to review the past. But I believe Google has a good chance of being a 5,000% gainer. Check with me in 10 years and we'll see how it turned out.

Disclosure: at the time of this posting the author was long MSFT and GOOG.

Microsoft provides a good case study. Microsoft peaked at $58 and change right at the end of 1999. Then came the collapse of the tech bubble. Microsoft has done nothing but go sideways for seven years. Finally on Friday Microsoft hit a six year high of $35 after reporting a superb quarter that showed all lines of business were executing exceptionally well.

Microsoft IPO'd about 1985. On a split adjusted basis a share of stock was worth 9.5 cents. From that point to the peak is a return of 6,110%. Many times people look at a stock that has moved strongly from the lower right to the upper left and feel that they've "missed the boat". If you'd bought Microsoft at the beginning of 1990 a share would have cost about $0.64. The stock would already have gone up 670%. But you would still have made a 910% return at the peak. If you bought Microsoft in 1995 a share would have cost $3.71 on a split adjusted basis. Over the next 5 years you would have a return of almost 160%, or an annualized return of 32% a year.

Somewhere today there is the next 5,000% stock. While hindsight is entertaining it is not particularly profitable. What are the characteristics of a stock that can return 5,000% over 15 or 20 years?

In the case of Microsoft it was a defensible franchise in a fast growing industry, personal computers. Microsoft's operating system dominance meant that they grew as the industry grew. Many additional products put out by Microsoft over the years, such as Microsoft Office and Internet Explorer, have been successful and profitable in their own right, but essentially were developed to protect the core operating system franchise.

I own a lot of different stocks and I own them for a lot of different reasons. But of all the stocks I own the one that I think may turn in a Microsoft performance over the next 10 years is Google. Google IPO'd 3 years ago for $85 a share. I first bought Google in late 2006 for $410. At that time Google had already posted a return of 482%. Friday, Google's closing price was $674.60, representing an increase of 794% since the IPO.

Google has not split its shares and the high stock price along with concerns over the sustainability of its growth have meant that the shares have climbed a "wall of worry" and moved up in a rational way based on its continued strong earnings. The stock remained fairly flat last year and early this year. But with the latest quarter analysts are starting to become more comfortable that growth and earnings are not going to slow down precipitously - at least not in the foreseeable future.

Like Microsoft, Google has a dominate position and a defensible franchise in an industry that is expect to grow for a long time - search and Internet advertising. Google's search algorithms continue to improve and this latest quarter showed financial gains based on more accurately targeted advertising based on search results.

Like Microsoft, Google's business model generates huge amounts of free cash flow. This gives Google the ability to invest in widening its moat and invest in other products and services for future growth. Google has its fingers in a lot of pies, but they have been disciplined in that most of these initiatives are either meant to defend the core franchise (like Microsoft realizing that it had to win the Internet browser war), or meant to expand its footprint within the scope of it's stated mission. That mission is to organize the world's information and monetize the access of that information. There has been no move by Google that just doesn't fit, like Ebay's acquisition of Skype (which Ebay just took a massive write-down on).

Google is a global growth story with about 50% of its revenue coming from outside the United States. Google continues to gain market share in almost every market in which they compete. They are even gaining market share in the U.K. where their market share is already 70%.

It is much harder to see the future than to review the past. But I believe Google has a good chance of being a 5,000% gainer. Check with me in 10 years and we'll see how it turned out.

Disclosure: at the time of this posting the author was long MSFT and GOOG.

Thursday, October 25, 2007

Airline Arrogance

The federal government is threatening to impose hard caps on the number of flights, including Delta flights, that can be scheduled for JFK airport in New York City. One third of the flights out of JFK are either canceled or delayed. The airlines insist on flight schedules that are impossible to maintain even in the best of circumstances. The airlines are aghast that caps may be imposed and have sworn to fight this with every ounce of energy they can muster.

I saw the CEO and Chairman of United Airlines interviewed today on one of the business news channels. When challenged about the unrealistic flight schedules and chronic flight delays was his answer to accept any responsibility? No. His response was that they scheduled flights when people want to fly and if the air traffic control and airport infrastructure can not accommodate those flights then it is their fault - not the fault of the airlines.

This is a great example of the way in which airlines combine arrogance and incompetence. As a frequent Gold member of Delta's frequent flier program I know only too well about the vagaries of unrealistic flight schedules, canceled flights and poorly maintained planes.

The airline industry has been the greatest destroyer of shareholder value of any industry sector of the last century, and I suspect it will continue to do so.

I saw the CEO and Chairman of United Airlines interviewed today on one of the business news channels. When challenged about the unrealistic flight schedules and chronic flight delays was his answer to accept any responsibility? No. His response was that they scheduled flights when people want to fly and if the air traffic control and airport infrastructure can not accommodate those flights then it is their fault - not the fault of the airlines.

This is a great example of the way in which airlines combine arrogance and incompetence. As a frequent Gold member of Delta's frequent flier program I know only too well about the vagaries of unrealistic flight schedules, canceled flights and poorly maintained planes.

The airline industry has been the greatest destroyer of shareholder value of any industry sector of the last century, and I suspect it will continue to do so.

Rangel Wrangles the Tax Code Mess

It is hard not to like Congressman Charlie Rangel. He is engaging, likable, self-depreciating and he always spins a great story. As I watched him outline his tax reform proposal today I found myself being drawn in. Then I looked at the details.

Fixing the AMT must be done. This part is not in question. The AMT was imposed decades ago to address about a dozen very wealthy taxpayers that followed the tax code of the day but did not pay income taxes. The AMT was to make sure these taxpayers paid taxes no matter what. In the grand tradition of the U.S. Congress they screwed it up. The bill was not indexed for inflation. Over the years the AMT dragnet has ensnared more an more taxpayers, reaching well down into the middle class. Without at least a temporary fix something like 27M taxpayers will have to pay the AMT. That is a lot more than 12.

The AMT represents money that was never meant to be collected by the government. So by repealing the tax why do we have to raise other taxes to replace it? It was a mistake. Just repeal it and move on. But that's not the way the government works. They can't do without the money, but they believe you can do without the money.

Another item that Charlie Rangel wants to address is to lower the corporate income tax to a level where American companies are on par with their foreign competitors. He also want to provide more benefits to lower and middle income families.

I'm not going to get into the semantics of a "surcharge" on the rich verse a higher tax rate. I'll just do the math and let the numbers fall where they may.

For individuals making more than $150,000, or families making more than $200,000 the top marginal tax rate will increase 26% from 35% to 44%. This means that the top rate will translate into taking home 56 cents of every dollar instead of 65 cents of every dollar. It also means that there will be a huge marriage penalty for filing jointly.

The top corporate tax rate will be lowered to 30.5%. This makes us somewhat more competitive with the rest of the world; at least a step in the right direction. Corporations don't really pay taxes anyway. Individuals end up paying all the taxes at the end of the day.

A tax break to encourage manufacturing in the U.S. will be repealed. This tax break was just passed by the Democrats a couple of years ago over the objection of President Bush. Now they don't like it.

Another big tax increase will be on so called "carried interest", or the payments made to private equity and hedge fund managers based on capital gains in the funds they manage (no gains, no payment). Most other developed countries (U.K., France, Spain, etc. all treat carried interest as capital gains). This will raise the tax on long term capital gains for these individuals from 15% to 44%. This proposal will undoubtedly drive capital away from the U.S.

The beneficiaries of this massive tax hike ($1 trillion dollars minimum over 10 years) will include an expansion of the people that receive the earned income tax credit. Now this isn't really a tax cut. The people receiving this benefit don't pay taxes. We'll just write more people checks.

Many other people will receive additional tax breaks and benefits, such as through an expansion of the standard deduction by $850.

The end result is a very large tax increase on small businesses and capital investment. These are the elements of our economy that create the jobs for everyone else. To increase taxes just when the economy is slowing, hopefully to a soft landing, if the height of irresponsibility. It almost guarantees a recession.

But if your a Democrat and sorely desire that the next Presidential administration be a Democratic Administration having a soft landing is not politically beneficial to you. Harming the economy instead while at the same time buying votes through a massive redistribution of income sounds pretty good.

The Bush tax cuts and pro-growth policies have created jobs, grown real wages and delivered a surge of revenue into the federal coffers resulting in a historically low deficit. Charlie Rangel's plan would constitute the largest tax increase in U.S. history and a transfer of wealth on a massive scale.

I do think Charlie Rangel deserves some credit. He knows that this proposal will not be the final answer but he has put out a position that can be debated and molded. It is a complex issue. But I hope we end up promoting a strong economy that benefits all and not just punishing success.

Fixing the AMT must be done. This part is not in question. The AMT was imposed decades ago to address about a dozen very wealthy taxpayers that followed the tax code of the day but did not pay income taxes. The AMT was to make sure these taxpayers paid taxes no matter what. In the grand tradition of the U.S. Congress they screwed it up. The bill was not indexed for inflation. Over the years the AMT dragnet has ensnared more an more taxpayers, reaching well down into the middle class. Without at least a temporary fix something like 27M taxpayers will have to pay the AMT. That is a lot more than 12.

The AMT represents money that was never meant to be collected by the government. So by repealing the tax why do we have to raise other taxes to replace it? It was a mistake. Just repeal it and move on. But that's not the way the government works. They can't do without the money, but they believe you can do without the money.

Another item that Charlie Rangel wants to address is to lower the corporate income tax to a level where American companies are on par with their foreign competitors. He also want to provide more benefits to lower and middle income families.

I'm not going to get into the semantics of a "surcharge" on the rich verse a higher tax rate. I'll just do the math and let the numbers fall where they may.

For individuals making more than $150,000, or families making more than $200,000 the top marginal tax rate will increase 26% from 35% to 44%. This means that the top rate will translate into taking home 56 cents of every dollar instead of 65 cents of every dollar. It also means that there will be a huge marriage penalty for filing jointly.

The top corporate tax rate will be lowered to 30.5%. This makes us somewhat more competitive with the rest of the world; at least a step in the right direction. Corporations don't really pay taxes anyway. Individuals end up paying all the taxes at the end of the day.

A tax break to encourage manufacturing in the U.S. will be repealed. This tax break was just passed by the Democrats a couple of years ago over the objection of President Bush. Now they don't like it.

Another big tax increase will be on so called "carried interest", or the payments made to private equity and hedge fund managers based on capital gains in the funds they manage (no gains, no payment). Most other developed countries (U.K., France, Spain, etc. all treat carried interest as capital gains). This will raise the tax on long term capital gains for these individuals from 15% to 44%. This proposal will undoubtedly drive capital away from the U.S.

The beneficiaries of this massive tax hike ($1 trillion dollars minimum over 10 years) will include an expansion of the people that receive the earned income tax credit. Now this isn't really a tax cut. The people receiving this benefit don't pay taxes. We'll just write more people checks.

Many other people will receive additional tax breaks and benefits, such as through an expansion of the standard deduction by $850.

The end result is a very large tax increase on small businesses and capital investment. These are the elements of our economy that create the jobs for everyone else. To increase taxes just when the economy is slowing, hopefully to a soft landing, if the height of irresponsibility. It almost guarantees a recession.

But if your a Democrat and sorely desire that the next Presidential administration be a Democratic Administration having a soft landing is not politically beneficial to you. Harming the economy instead while at the same time buying votes through a massive redistribution of income sounds pretty good.

The Bush tax cuts and pro-growth policies have created jobs, grown real wages and delivered a surge of revenue into the federal coffers resulting in a historically low deficit. Charlie Rangel's plan would constitute the largest tax increase in U.S. history and a transfer of wealth on a massive scale.

I do think Charlie Rangel deserves some credit. He knows that this proposal will not be the final answer but he has put out a position that can be debated and molded. It is a complex issue. But I hope we end up promoting a strong economy that benefits all and not just punishing success.

Invested in Failure

There was not a single civilian or military casualty in Iraq’s Anbar Province last week. This seems like a big milestone. It has not been reported in the NYT’s or NBC or any of the other liberal media outlets. Amazing, but it makes sense. If the situation continues to improve in Iraq it will hurt the chances for a Democratic administration.

I just watched a video of a couple of Democratic Congressmen being interviewed prior to the Petreaus hearings. The interviewer asked the Congressmen what would it mean if General Petreaus was able to testify in September that the security situation was improving? The Congressmen responded, “That would be a big problem for us.”

The Democrats are so invested in failure they don’t know how to react when we succeed.

I just watched a video of a couple of Democratic Congressmen being interviewed prior to the Petreaus hearings. The interviewer asked the Congressmen what would it mean if General Petreaus was able to testify in September that the security situation was improving? The Congressmen responded, “That would be a big problem for us.”

The Democrats are so invested in failure they don’t know how to react when we succeed.

Wednesday, October 24, 2007

Home Depot - My Most Frustrating Stock

I've lost more money on other stocks. In fact, I've been complicit in some spectacular collapses. Nevertheless perhaps my most frustrating stock of all time is Home Depot. I purchased Home Depot in 2000 for about $48 a share. It closed today for $30.88. Unfortunately it is in an account that is a hassle to access and expensive to trade so I've left it in there hoping for an eventually turnaround.

The last seven years have been a chamber of horrors. Bernie Marcus and Arthur Blank wisely understood that for Home Depot to reach the next stage they needed to bring in a top flight CEO. Unfortunately they hired Bob Nardelli instead.

Actually Bob Nardelli did some good things operationally that were needed. He brought disciple to the supply chain. He simplified the management structure. But he also destroyed a very positive culture and under invested in the stores. Bob Nardelli was no merchant.

I was actually supportive of Mr. Nardelli's expansion into the commercial supply business. Thinking like the GE trained executive he was he saw an opportunity to leverage Home Depots' improved supply chain and enormous purchasing power.

But all of those commercial supply assets were purchased at top dollar. With Nardelli gone Home Depot began to dismantle his industrial vision to return to its shopkeeper roots. But now those assets were unloaded at bargain basement prices. The money was supposed to go a long way toward a massive stock buyback that was going to finally get the shares moving. But they screwed even that up. The price of Home Depot Supply had to be lowered even more and the share buyback was diluted as a result.

Just prior to Nardelli getting the boot its was rumored that Home Depot could be taken out in a private equity deal. To deter this Nardelli immediately leveraged up the balance sheet by issuing a huge bond offering lowering the company's credit rating.

Nardelli's crowning achievement in arrogance was the infamous stockholder meeting. I won't recount the whole sordid tale but I've never seen anything like it. It was clear that Nardelli was going out of his way to tell the shareholders that he could care less what they thought.

The big countdown clock limiting shareholder comments to just a few minutes each combined with the security goons dressed in orange Home Depot aprons was something out of a bad movie. If a shareholder ran over their 2 minutes the microphone was turned off and the security thugs began moving in to silence the share owning corporate interlopers.

Now Home Depot Supply has been sold off in a fire sale. The balance sheet is loaded with debt. The Home Depot landscaping supply business is being shut down. The Home Depot Expo high end stores have never moved beyond a hobby. The sharp downturn in the housing industry is adding insult to injury.

It is finally time to bite the bullet, sell this dog, and continue shopping at Lowes.

Disclosure: at the time of this posting the author was long HD.

The last seven years have been a chamber of horrors. Bernie Marcus and Arthur Blank wisely understood that for Home Depot to reach the next stage they needed to bring in a top flight CEO. Unfortunately they hired Bob Nardelli instead.

Actually Bob Nardelli did some good things operationally that were needed. He brought disciple to the supply chain. He simplified the management structure. But he also destroyed a very positive culture and under invested in the stores. Bob Nardelli was no merchant.

I was actually supportive of Mr. Nardelli's expansion into the commercial supply business. Thinking like the GE trained executive he was he saw an opportunity to leverage Home Depots' improved supply chain and enormous purchasing power.

But all of those commercial supply assets were purchased at top dollar. With Nardelli gone Home Depot began to dismantle his industrial vision to return to its shopkeeper roots. But now those assets were unloaded at bargain basement prices. The money was supposed to go a long way toward a massive stock buyback that was going to finally get the shares moving. But they screwed even that up. The price of Home Depot Supply had to be lowered even more and the share buyback was diluted as a result.

Just prior to Nardelli getting the boot its was rumored that Home Depot could be taken out in a private equity deal. To deter this Nardelli immediately leveraged up the balance sheet by issuing a huge bond offering lowering the company's credit rating.

Nardelli's crowning achievement in arrogance was the infamous stockholder meeting. I won't recount the whole sordid tale but I've never seen anything like it. It was clear that Nardelli was going out of his way to tell the shareholders that he could care less what they thought.

The big countdown clock limiting shareholder comments to just a few minutes each combined with the security goons dressed in orange Home Depot aprons was something out of a bad movie. If a shareholder ran over their 2 minutes the microphone was turned off and the security thugs began moving in to silence the share owning corporate interlopers.

Now Home Depot Supply has been sold off in a fire sale. The balance sheet is loaded with debt. The Home Depot landscaping supply business is being shut down. The Home Depot Expo high end stores have never moved beyond a hobby. The sharp downturn in the housing industry is adding insult to injury.

It is finally time to bite the bullet, sell this dog, and continue shopping at Lowes.

Disclosure: at the time of this posting the author was long HD.

The Alchemists of Wall Street

The practitioners of technical analysis are the alchemists of our modern financial world, attempting to conjure gold out of stock charts. Whole careers have been made out of calling out buy and sell signals based on this line crossing that line and the like without regard to the fundamentals or economic cycles. Does it work? Sometimes it does.

Does it work because it is true, or because people believe it is true and therefore act on it? I believe that more often than not it is self-fulfilling prophecy. People believe in it and trade based on it so it becomes true. I suppose in some ways it is a way of understanding one element of investor psychology.

The result is that you have to pay attention to it, because so many people ascribe to it and buy and sell based on it. But do I think that the dreaded "double top" is all powerful? Not really. Like the alchemists of old, technical traders are always trying to find that "system" or "formula" that is guarranteed to make them money without having to understand the underlying company. It apparently is seductive because almost all of the adds I see on CNBC for trading systems are marketed on this basis. Many newletters are based on one flavor or another of technical analysis too.

I invest and trade based on fundamentals, the economic cycle, psychology and yes, technicals. But I take it with a grain of salt.

Does it work because it is true, or because people believe it is true and therefore act on it? I believe that more often than not it is self-fulfilling prophecy. People believe in it and trade based on it so it becomes true. I suppose in some ways it is a way of understanding one element of investor psychology.

The result is that you have to pay attention to it, because so many people ascribe to it and buy and sell based on it. But do I think that the dreaded "double top" is all powerful? Not really. Like the alchemists of old, technical traders are always trying to find that "system" or "formula" that is guarranteed to make them money without having to understand the underlying company. It apparently is seductive because almost all of the adds I see on CNBC for trading systems are marketed on this basis. Many newletters are based on one flavor or another of technical analysis too.

I invest and trade based on fundamentals, the economic cycle, psychology and yes, technicals. But I take it with a grain of salt.

How Dry is the Desert?

I've seen several stories and comments by the likes of CNN and Harry Reid about how the fires in Southern California are the result of global warming and that we are entering a long term period of conflagration. The rationale is that global warming is making Southern California and the Los Angeles area too dry.

OK, let's break this down. Many people don't know that Los Angeles is in the middle of a desert. In fact, the only reason a city can even exist there is that an entire major river was re-routed from the Sierra-Nevada mountains to Los Angeles to provide water.

I hate to disappoint Senator Reid, but deserts are DRY, global warming or not. Being from Nevada Harry Reid should understand this but unfortunately he often struggles with basic concepts.

The hot, dry Santa Anna winds that are fanning the flames are a long standing weather phenomenon that often occur this time of year - and have since time immemorial.

Now there are reports that some of the fires were deliberately set. Perhaps the arsonists were global warming warriors trying to "fan the flames" of this controversial issue.

OK, let's break this down. Many people don't know that Los Angeles is in the middle of a desert. In fact, the only reason a city can even exist there is that an entire major river was re-routed from the Sierra-Nevada mountains to Los Angeles to provide water.

I hate to disappoint Senator Reid, but deserts are DRY, global warming or not. Being from Nevada Harry Reid should understand this but unfortunately he often struggles with basic concepts.

The hot, dry Santa Anna winds that are fanning the flames are a long standing weather phenomenon that often occur this time of year - and have since time immemorial.

Now there are reports that some of the fires were deliberately set. Perhaps the arsonists were global warming warriors trying to "fan the flames" of this controversial issue.

Facebook Folly

Microsoft just announced that they signed a definitive agreement to take a stake in Facebook for $240M. A complete acquisition of Facebook by Microsoft is being valued at $15B, with a "B".

Facebook is reported to have revenues of $150M and profits of $30M. That means that Microsoft is paying 100 times sales. Madness.

The other company bidding for Facebook was Google. I suspect that Google would have been glad to acquire Facebook for a reasonable price but instead probably bid up the company to force Microsoft to pay top dollar.

Is there a wisp of desperation in the air as Microsoft trys to be "cool" and relevant to the younger generation, a position that was long ago lost to the the likes of Apple and Google?

Disclosure: at the time of this posting the author was long MSFT, APPL and GOOG.

Facebook is reported to have revenues of $150M and profits of $30M. That means that Microsoft is paying 100 times sales. Madness.

The other company bidding for Facebook was Google. I suspect that Google would have been glad to acquire Facebook for a reasonable price but instead probably bid up the company to force Microsoft to pay top dollar.

Is there a wisp of desperation in the air as Microsoft trys to be "cool" and relevant to the younger generation, a position that was long ago lost to the the likes of Apple and Google?

Disclosure: at the time of this posting the author was long MSFT, APPL and GOOG.

Monday, October 22, 2007

Apple Crushes Earnings

Apple just released 4th quarter earnings. Even with Apple's characteristic sandbagging, the numbers where absolutely huge. The company earned $1.01 vs. analysts estimates of $0.86. Apple beat on the top line as well. Some highlights of the most important points:

Disclosure: at the time of this posting the author was long AAPL.

- Profits increased 67% year over year.

- Raised guidance for the next quarter. This is quite significant due to the fact that Apple is always very conservative with guidance.

- Sold 1.2M iPhones and more than 10M iPods. This is important because iPod growth continues at 18%, iPhones exceeded expectations, and the iPod does not appear to be cannibalizing iPod sales.

- iPod market share is lower outside of the U.S. meaning that there is a lot of growth potential internationally.

- iPhone will be launched in Europe and the U.K. soon.

- Apple continues to have an extremely strong balance sheet with $15B in cash and zero debt.

- Apple sold more than 2M Macintosh computers for the first time in its history. Apple might have taken "computer" off of their name but it is still a very large driver of revenues and profits.

- Apple's new operating system, "Leopard", begins shipping on Friday.

- Perhaps most important, gross margin for the quarter was 33.6%, up from 29.2% the previous year. That is vastly better than Apple’s competitors in either the computer or cellphone industries.

Disclosure: at the time of this posting the author was long AAPL.

Sunday, October 21, 2007

Oil - Slip Slidin' Away

Rising oil prices can be either positive or negative depending on the reason for the high price. High oil prices due to a shortage or production and supply can be catastrophic. Currently there is enough oil production, albeit with not a large margin for error. But in fact world oil production is increasing and inventories are robust. In fact, oil prices have risen due to the strong, synchronized economic growth around the world. This strong growth is extremely positive and can absorb high oil prices.

Oil topped $90 a barrel last week. In no way do the fundamentals of supply and demand support $90 oil. There continues to be a $15 to $20 terror premium on the price of a barrel of oil. But even backing out the terror premium oil is still too high.

Tensions between Turkey and Kurdish radicals in northern Iraq continue to be extremely high. Secretary Rice has managed to get Turkey to hold off on military intervention in northern Iraq - for now.

Hopefully Nancy Pelosi's stupidly lame attempt at foreign policy with her "Armenian Gambit" will not inflame matters further than than it already has. Perhaps Nancy does not know that an important oil pipeline transporting oil from Iraq runs through Kurdish Iraq and Turkey. Perhaps she also does not know that the heavy armored vehicles needed by our soldiers are reaching Iraq primarily over land routes through our NATO partner Turkey. Perhaps she does not know that the Ottoman Empire no longer exists.

Barrons this week highlights an opinion by Oppenheimer & Company that argued oil prices are primed for a downturn. They also anticipate that an attack on Iraq by the United States could come within a number of months. Of course this would result in a spike in oil, but as Oppenheimer stated, "Iran needs oil export revenues more than the world needs its oil exports."

I am strongly considering shorting oil via the USO ETF Monday and perhaps shorting Exxon as well. I believe oil has overreached and is due for a pullback.

I am also hopeful that refining margins will improve. After a nice move up after the late summer lows refiners have pulled back a bit. Cracking spreads are under pressure because gas prices have not kept up with oil prices. A pullback in oil could actually increase cracking spreads and give a lift to refiners. The period from September to June is historically the be time to own refiners.

Disclosure: at the time of this posting the author was long DVN, VLO and TSO.

Oil topped $90 a barrel last week. In no way do the fundamentals of supply and demand support $90 oil. There continues to be a $15 to $20 terror premium on the price of a barrel of oil. But even backing out the terror premium oil is still too high.

Tensions between Turkey and Kurdish radicals in northern Iraq continue to be extremely high. Secretary Rice has managed to get Turkey to hold off on military intervention in northern Iraq - for now.

Hopefully Nancy Pelosi's stupidly lame attempt at foreign policy with her "Armenian Gambit" will not inflame matters further than than it already has. Perhaps Nancy does not know that an important oil pipeline transporting oil from Iraq runs through Kurdish Iraq and Turkey. Perhaps she also does not know that the heavy armored vehicles needed by our soldiers are reaching Iraq primarily over land routes through our NATO partner Turkey. Perhaps she does not know that the Ottoman Empire no longer exists.

Barrons this week highlights an opinion by Oppenheimer & Company that argued oil prices are primed for a downturn. They also anticipate that an attack on Iraq by the United States could come within a number of months. Of course this would result in a spike in oil, but as Oppenheimer stated, "Iran needs oil export revenues more than the world needs its oil exports."

I am strongly considering shorting oil via the USO ETF Monday and perhaps shorting Exxon as well. I believe oil has overreached and is due for a pullback.

I am also hopeful that refining margins will improve. After a nice move up after the late summer lows refiners have pulled back a bit. Cracking spreads are under pressure because gas prices have not kept up with oil prices. A pullback in oil could actually increase cracking spreads and give a lift to refiners. The period from September to June is historically the be time to own refiners.

Disclosure: at the time of this posting the author was long DVN, VLO and TSO.

Saturday, October 20, 2007

Krauthammer's Razor

There are lots of fuzzy minded op-end columnists out there. Others are just angry. Perhaps they weren't held enough as children. But Charles Krauthammer is not one of them. He is thoughtful and reasoned and provides interesting insights into the strange world inside the Washington, D.C. beltway where normal thought processes and common sense rarely come into play.

Mr. Krauthammer's latest column focuses on Nancy Pelosi's "Armenian Gambit". I especially liked "Krauthammer's Razor". The last paragraph reads as follows:

"Is the Armenian resolution her way of unconsciously sabotaging the U.S. war effort, after she had failed to stop it by more direct means? I leave that question to psychiatry. Instead, I fall back on Krauthammer's razor (with apologies to Occam): In explaining any puzzling Washington phenomenon, always choose stupidity over conspiracy, incompetence over cunning. Anything else gives them too much credit. "

Well said. He also provides some very interesting historical context regarding America's humanitarian assistance during the Ottoman/Armenian tradgey.

How badly do you have to bungle something to have John Murtha, Democratic Party thug in residence and Abscam unindicted co-conspirator, back away and say that you're making a mistake. Ouch.

http://www.washingtonpost.com/wp-dyn/content/article/2007/10/18/AR2007101801579_2.html

Mr. Krauthammer's latest column focuses on Nancy Pelosi's "Armenian Gambit". I especially liked "Krauthammer's Razor". The last paragraph reads as follows:

"Is the Armenian resolution her way of unconsciously sabotaging the U.S. war effort, after she had failed to stop it by more direct means? I leave that question to psychiatry. Instead, I fall back on Krauthammer's razor (with apologies to Occam): In explaining any puzzling Washington phenomenon, always choose stupidity over conspiracy, incompetence over cunning. Anything else gives them too much credit. "

Well said. He also provides some very interesting historical context regarding America's humanitarian assistance during the Ottoman/Armenian tradgey.

How badly do you have to bungle something to have John Murtha, Democratic Party thug in residence and Abscam unindicted co-conspirator, back away and say that you're making a mistake. Ouch.

http://www.washingtonpost.com/wp-dyn/content/article/2007/10/18/AR2007101801579_2.html

Friday, October 19, 2007

Masters of the Obvious

Wall Street stock analysts are sometimes helpful but more often are suspect. I won't rehash the many ethical lapses of this industry leading up to the collapse of the Nasdaq and the stock market in general in 2000. Hundreds of millions of dollars of fines were imposed but I wonder how much better it is.

One of the new rules was put in place due to the grivious conflicts of interest with firms recommending stocks for whom they sought or performed investment banking services. The firms are required to disclose if the have or are actively seeking investment banking business with a company for which they provide stock market analysis and recommendations.

How do these Wall Street firms implement this regulation? They simply slap a disclaimer at the bottom of every stock report stating that they may be seeking or intend to seek investment banking work with that respective company. The same statement on every company report. So I don't know any more before I did in 2000.

Through my several brokerage accounts I have access to a number of reports including those from Charles Schwab, Standard & Poor, Merrill Lynch, Goldman Sachs and Morningstar among others.

An exception to the independence issue is Morningstar, since they do not have an investment banking line of business. They have an interesting methodolgy that is very Warren Buffett like. They strongly favor companies with a defensible franchise, or moat. I find that Morningstar is often in disagreement with the other brokerage recommendations on both the buy and the sell side.

Disclosure: at the time of this posting the author was long LFC.

One of the new rules was put in place due to the grivious conflicts of interest with firms recommending stocks for whom they sought or performed investment banking services. The firms are required to disclose if the have or are actively seeking investment banking business with a company for which they provide stock market analysis and recommendations.

How do these Wall Street firms implement this regulation? They simply slap a disclaimer at the bottom of every stock report stating that they may be seeking or intend to seek investment banking work with that respective company. The same statement on every company report. So I don't know any more before I did in 2000.

Through my several brokerage accounts I have access to a number of reports including those from Charles Schwab, Standard & Poor, Merrill Lynch, Goldman Sachs and Morningstar among others.

An exception to the independence issue is Morningstar, since they do not have an investment banking line of business. They have an interesting methodolgy that is very Warren Buffett like. They strongly favor companies with a defensible franchise, or moat. I find that Morningstar is often in disagreement with the other brokerage recommendations on both the buy and the sell side.

One of my frustrations with Morningstar, however, is that as far as I can tell they will not recommend companies in highly cyclical industries. Some of the greatest investing profits can be made in cyclical industries as the normal economic cycles wax and wane.

I do not find Merrill Lynch particularly helpful. I find Goldman Sachs quite good and I trust Goldman Sachs' insight and judgement more than most. When Goldman puts a stock on their "Conviction Buy" list I pay attention. Charles Schwab's rating system seems to mostly be about momentum, and the ratings change a lot. Stocks making strong moves up are upgraded and visa versa, perhaps encouraging more frequent trading and therefore fees to Charles Schwab.